Futures Market: Last Friday night, LME copper opened at $8,806/mt, initially dipping to $8,791.5/mt before fluctuating upward throughout the session, peaking at $8,908/mt near the close, and finally settling at $8,893.5/mt, up 1.05%. Trading volume reached 16,900 lots, and open interest stood at 261,000 lots. On the same night, the most-traded SHFE copper 2502 contract opened at 73,230 yuan/mt, initially dipping to 73,160 yuan/mt before surging to an intraday high of 73,850 yuan/mt. It then pulled back slightly and fluctuated rangebound near the close, ultimately settling at 73,810 yuan/mt, up 1.08%. Trading volume reached 34,300 lots, and open interest stood at 154,000 lots.

【SMM Copper Morning Brief】News: (1) In December, the US ISM Manufacturing PMI recorded 47.4, slightly above the market expectation of 47.1 and up 0.7 points from the previous reading of 46.7. However, it remained in contraction territory for the 14th consecutive month. Since June, the PMI has been fluctuating within a narrow range at the bottom.

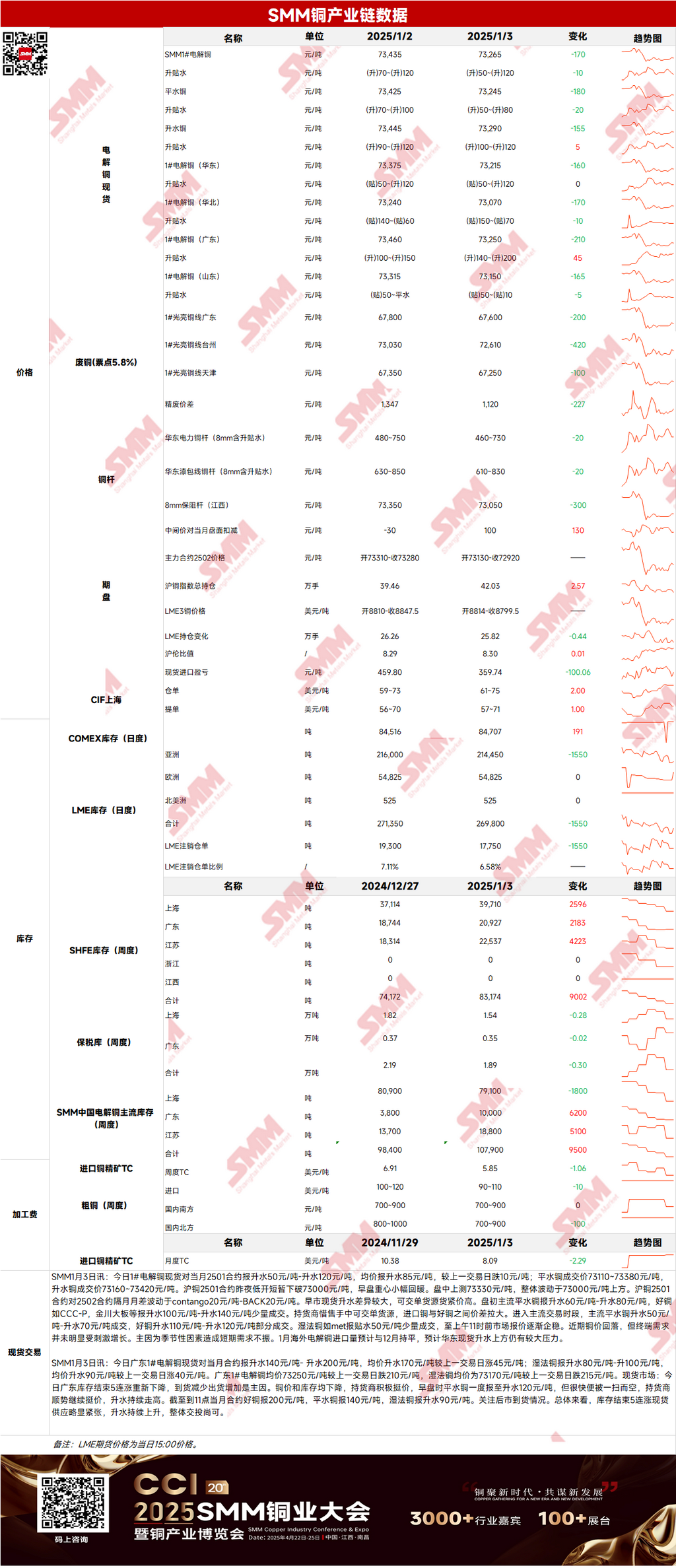

Spot Market: (1) Shanghai: On January 3, mainstream standard-quality copper spot premiums against the front-month contract were quoted at 50-80 yuan/mt, while high-quality copper was quoted at 100-120 yuan/mt. Although copper prices have pulled back recently, end-use demand has not shown significant growth, mainly due to seasonal factors causing short-term demand weakness. The import volume of overseas copper cathode in January is expected to remain flat compared to December, and spot premiums in east China are expected to face significant resistance at higher levels.

(2) Guangdong: On January 3, #1 copper cathode spot premiums against the front-month contract in Guangdong were quoted at 140-200 yuan/mt, with an average premium of 170 yuan/mt, up 45 yuan/mt from the previous trading day. Hydro copper was quoted at 80-100 yuan/mt, with an average premium of 90 yuan/mt, up 40 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 73,250 yuan/mt, down 210 yuan/mt from the previous trading day, while hydro copper averaged 73,170 yuan/mt, down 215 yuan/mt. Overall, inventories ended a five-day increase, and spot supply appeared slightly tight, driving premiums to continue rising.

(3) Imported Copper: On January 3, warehouse warrant prices ranged from $61 to $75/mt (QP January), with the average price up $2/mt from the previous trading day. B/L prices ranged from $57 to $71/mt (QP February), with the average price up $1/mt from the previous trading day. EQ copper (CIF B/L) was quoted at $12-26/mt (QP February), with the average price down $1/mt from the previous trading day. These quotes referenced cargoes arriving in late January and early February. A small number of transactions were recorded for both warehouse warrants and B/Ls during the day, with most deliveries concentrated before the holiday. Due to depleted bonded warehouse inventories, the center of gravity for warehouse warrant transactions shifted upward. Overall, with the execution of 2024 long-term contracts nearing completion, the market remained largely in a wait-and-see mode, and pre-holiday restocking activities were cautious.

(4) Secondary Copper: On January 3, secondary copper raw material prices fell by 200 yuan/mt MoM. Guangdong bare bright copper was priced at 67,500-67,700 yuan/mt, down 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,120 yuan/mt, down 227 yuan/mt MoM. The price spread between primary and secondary copper rods was 495 yuan/mt. According to an SMM survey, secondary copper raw material traders indicated that they would continue purchasing secondary copper raw materials overseas in the near term. Considering shipping schedules, arrivals are expected after the Chinese New Year, alleviating concerns about reduced capital efficiency during the holiday. Additionally, domestic scrap utilisation enterprises faced year-end financial constraints, and with lower purchase bids, suppliers were reluctant to sell excessive amounts of secondary copper raw materials.

(5) Inventory: On January 3, LME copper cathode inventories decreased by 1,550 mt to 269,800 mt. On December 19, SHFE warehouse warrant inventories decreased by 1,112 mt to 18,094 mt.

Prices: Macro side, last Friday, the State Council Information Office held a press conference on "China's High-Quality Economic Development Achievements," which boosted market sentiment. Looking ahead to this week, the US will release multiple labour market data points, and several US Fed officials are scheduled to speak. However, US data is unlikely to weaken the US dollar index at this stage, which will weigh on copper prices. Fundamentals side, although copper prices have remained low recently, end-use demand has not shown significant growth due to seasonal factors. Additionally, the import volume of overseas copper cathode in January is expected to remain flat compared to December, and spot premiums are expected to face pressure. In terms of prices, uncertainties surrounding US economic expectations remain significant. Although the US dollar index pulled back slightly last Friday, it is expected to fluctuate at highs. On the fundamentals side, the seasonal demand downturn is expected to deepen further, and copper prices are likely to face resistance at higher levels today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided herein is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】